In today's complex financial landscape, whether managing personal finances or steering the financial rudder of a thriving business, understanding the accounting cycle is crucial. The accounting cycle is a systematic process that ensures financial records are accurate, consistent, and useful for decision-making. This visual breakdown of the accounting cycle will demystify the sequence of steps involved, helping individuals and businesses maintain accuracy and integrity in their financial reporting.

The accounting cycle is composed of a series of repetitive steps designed to capture financial transactions and translate them into meaningful financial statements. It ensures that all financial actions are recorded consistently and can be reviewed, analyzed, and audited with ease. For individuals, this cycle can simplify personal finance management by providing a clear framework for tracking expenses and income. For businesses, mastering the accounting cycle is essential for fulfilling legal obligations, pursuing growth strategies, and maintaining stakeholder trust.

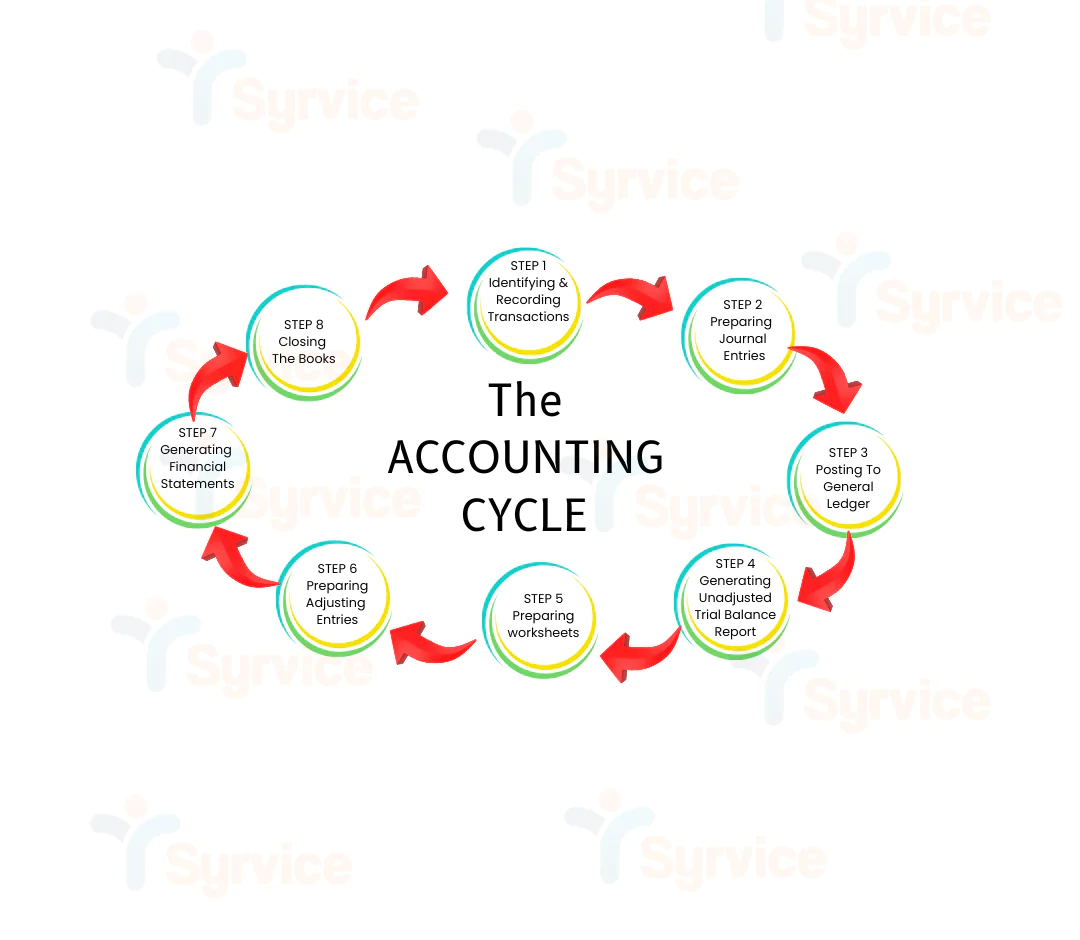

Transaction Identification and Recording:

The first step involves recognizing that a financial transaction has occurred. This includes all financial activities that affect the business or personal financial position. Each transaction is recorded in a journal, employing the double-entry accounting system, which ensures every entry is balanced by another.

Preparing Journal Entries:

Once transactions are identified, they are documented as journal entries. Each entry records the date, accounts affected, amounts debited or credited, and a brief description of the transaction. This foundation acts as a chronological record of all financial activity.

Posting to the General Ledger:

After journalizing, the next step involves transferring these entries to the general ledger. The ledger organizes transactions by account, providing a comprehensive view of each account's activity over time. This helps in monitoring accounts and preparing for the next stages of the cycle.

Generating Unadjusted Trial Balance Report:

A trial balance is prepared at the end of the accounting period, consolidating all the accounts to ensure total debits equal total credits. This step verifies the equality of the accounting equation (Assets = Liabilities + Equity), highlighting any discrepancies for correction.

Preparing Worksheets or Record Adjustments:

Adjusting entries are made to account for accrued expenses, unearned revenues, and other unrecorded financial activity that affects the period's financial outcomes. These adjustments offer a more accurate reflection of an entity’s financial status.

Preparing Adjusting Entries:

Once adjustments are made, an adjusted trial balance is prepared to confirm that all entries are accurate and in harmony. This serves as the foundation for financial statement preparation.

Generating Financial Statements:

From the adjusted trial balance, key financial statements are crafted. These include the income statement, balance sheet, and cash flow statement. These documents provide stakeholders a comprehensive view of the financial health and performance of the organization or individual.

Closing The Books:

The cycle concludes by closing temporary accounts, such as revenues and expenses, to the retained earnings account. This step resets these accounts to zero, preparing for the next accounting period. Closing entries ensure that income and expense accounts are appropriately aligned with the correct financial period.

Bonus Step.... Post-Closing Trial Balance:

The final step is preparing a post-closing trial balance to ensure all accounts are accurately represented after closing entries have been made. It serves as a final check to confirm that all debits and credits for permanent accounts are balanced.

The accounting cycle is essential for maintaining a robust financial management apparatus, providing a structured approach that enhances reliability and transparency of financial information. Whether you're managing your personal finances or overseeing a business's financial operations, understanding and applying the accounting cycle fosters better decision-making and financial health. By utilizing this visual breakdown, individuals and businesses can navigate the complexities of financial record-keeping with confidence and clarity, ensuring their accounts reflect a true and fair view of their financial position.